Fully occupied. Every tenant below market.

Anchor lease expires in two years.

What’s your take on this deal?

A few days ago, I posted a deal and asked what you’d offer. Here’s my take.

Those of you who have done a deal or two know that there is no such thing as a single correct price. Maybe a best estimate, but certainly not a sure-fire right answer. What if expenses grow faster than we projected? Or the exit cap rate compresses or expands? Or a meteor strikes your office and wipes out your hard drive? Stuff happens.

This solution presents a suggested offer of $875,000 and explains some of the reasoning behind it. You may come up with a different amount, and that’s ok – provided you have reasons you can explain.

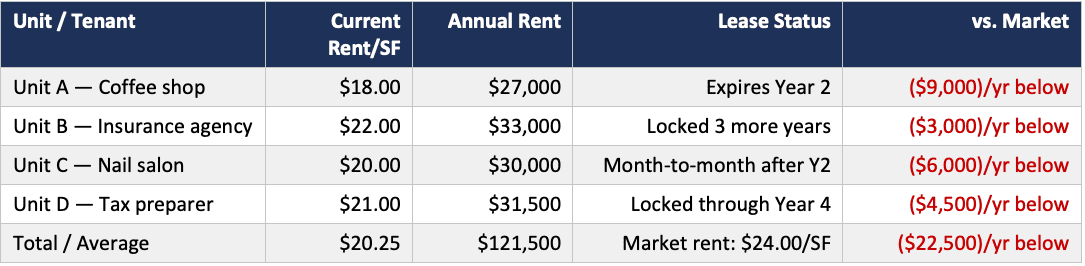

Start with what the rent roll is telling us

Before building a pro forma, we should examine the lease structure for what it tells us about risk and opportunity.

Every tenant is below market, and two of the four leases require attention within the first two years of your hold. That’s not a coincidence — it’s why this property will show a high entry cap rate at any reasonable asking price.

The cap rate isn’t a gift. It’s compensation for lease rollover risk.

Unit A is the one to watch. At $18/SF against a $24 market, it has the largest below-market spread in the building, and the lease expires at the end of Year 2. Unit C is already month-to-month. Units B and D are locked in and anchor your income stream.

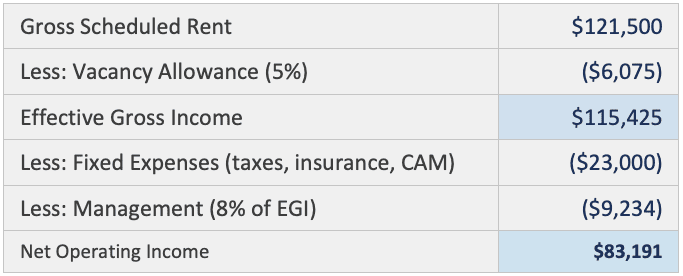

Year 1 NOI — before we pick a price

Calculating the NOI is usually a good place to start. The $3,000 CapEx reserve is contributed at closing and recovered at resale — so it’s not part of NOI, and it doesn’t reduce annual cash flow.

Deriving an offer price

Two approaches, used together.

Income capitalization: Comparable stabilized properties are trading at 7–8% cap rates. This property carries rollover risk, so a risk-adjusted cap of 8.5–9.5% seems appropriate:

- At 8.5%: $83,191 ÷ 0.085 = $978,718

- At 9.0%: $83,191 ÷ 0.090 = $924,344

- At 9.5%: $83,191 ÷ 0.095 = $875,694

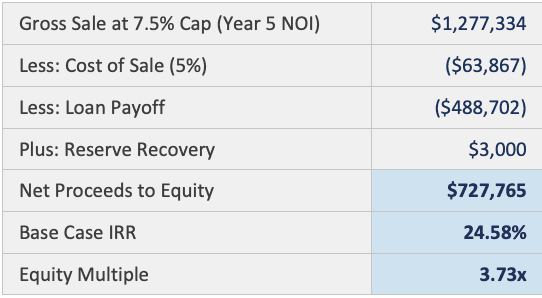

IRR targeting: For a value-add retail investment with meaningful lease rollover risk, a 15–20% leveraged IRR is a reasonable hurdle. At $875,000, the base case IRR is 24.58% — above the hurdle with room for the lease story to go sideways.

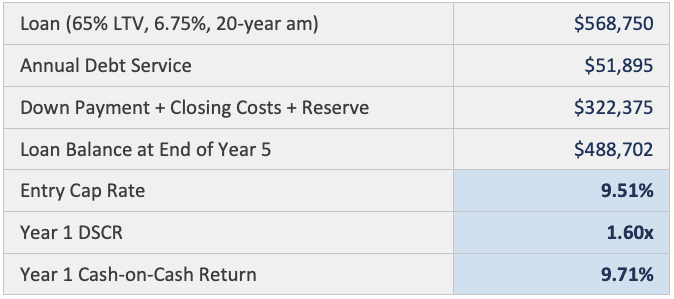

Financing at $875,000 purchase price

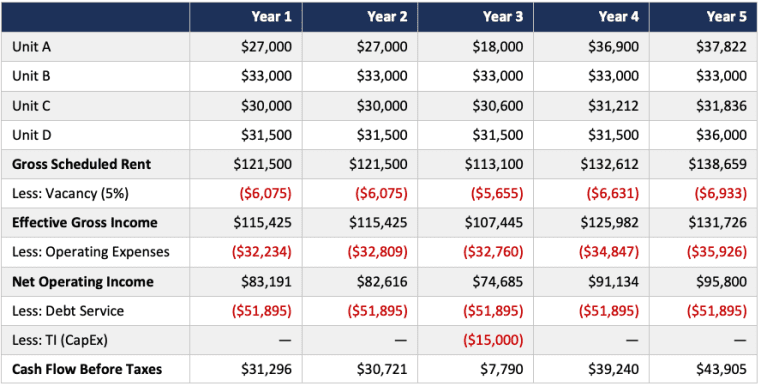

Base case pro forma

Here is where we need to think about this deal from the point of view of a real participant and make some realistic assumptions as to how our revenue and cash flow might play out.

- Unit A goes vacant for six months in Year 3 before re-leasing at market, with a $15,000 TI allowance charged as CapEx.

- Unit B’s lease is locked in through Year 4. We decide to hold Year 5 rent at $22/SF. At $2/SF below market, the tenant has a clear incentive to renew, and the conservative flat-rent assumption avoids overstating exit NOI.

- Unit C stays on modified month-to-month terms, averaging a 2% increase.

- Unit D renews at market in Year 5.

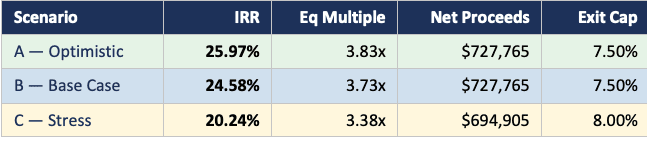

What if things go better — or worse?

We modeled the $875,000 price under three lease outcome assumptions:

The spread between optimistic and stress is about 5.7 percentage points — driven almost entirely by lease assumptions, not market conditions.

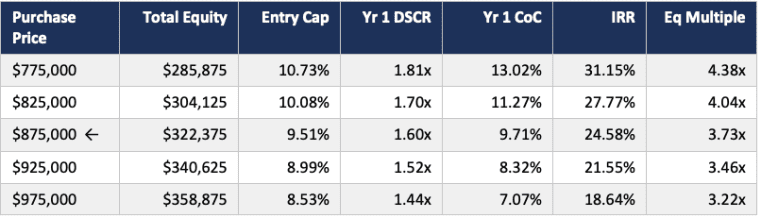

Sensitivity analysis

Price sensitivity (base case leases, 7.5% exit cap):

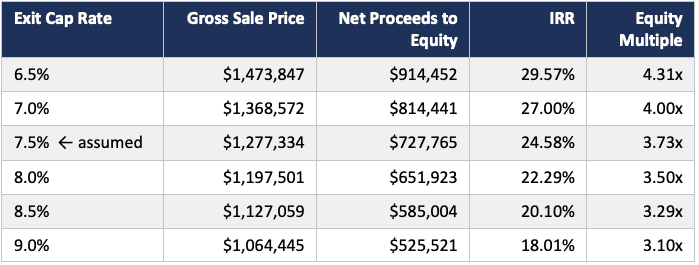

Exit cap rate sensitivity ($875,000, base case leases):

A 100 basis point expansion in the exit cap rate costs about 4.5 points of IRR. That’s a risk you can’t control — where cap rates are in five years.

The bottom line

At $875,000, this deal works under the base case assumptions, survives the stress scenario, and prices the lease rollover risk at roughly 150 basis points above market — appropriate given that two of four leases require negotiation within the first two years. The model rests on reasonable assumptions about how the lease events resolve, but the sensitivity tables above show exactly how much the outcome changes when those assumptions shift.

The natural temptation is to capitalize current NOI at the prevailing market cap rate and call that fair value. At prevailing market cap rates of 7–8%, that math produces a price between $1,040,000 and $1,109,000. The case for paying less comes down to one question: Is current NOI a reliable indicator of what this property will earn over the next five years? Given the lease structure, a careful underwriter would say it isn’t — not yet.

So our realistic bottom line is that our offer should be closer to $875,000, not the >$1 million suggested by simply capitalizing the NOI. We want to make our investment decision by looking at how the property might perform over our likely holding period, not just at a point in time.

This case is a somewhat simplified example of the kind of analysis I cover in Mastering Real Estate Investing — a comprehensive video course that grew out of more than a decade of my graduate-level teaching.

If you’d like to go deeper, the course covers pro forma modeling, financing, rate-of-return metrics, equity multiple, partnership structures, development, value-add, and case studies across multiple property types. You can find more details at learn.realdata.com.

Instructors who want to consider part or all of the content for classroom use can request complimentary evaluation access at https://real-estate-investor-education.teachable.com/p/university_curriculum.