Qualified Opportunity Zones:

Originally created under the 2017 tax act, the QOZ program was designed to spur investment in economically distressed areas by offering tax incentives for reinvesting capital gains through Qualified Opportunity Funds (QOFs). Under the new tax law, the program is now made permanent, and states will have the opportunity to re-designate zones every 10 years, starting in 2026.

One of the biggest updates is the move from a fixed capital gain recognition date to a more flexible, rolling five-year deferral. Under the new rules, if you reinvest capital gains into a Qualified Opportunity Fund (QOF) on or after January 1, 2027, you’ll defer the tax on that gain for five years from the date of your investment—rather than facing a hard deadline as in the original version of the law. The well-known 10-year holding period for excluding future appreciation is still in place, but investors now have more breathing room when it comes to timing. There are also added perks for rural zones, including a larger basis step-up and looser improvement requirements, which could make it easier to launch or expand real estate projects in those areas.

Section 1031 Tax-Deferred Exchange:

A like-kind exchange under Section 1031 allows real estate investors to defer capital gains taxes when they sell an investment property and reinvest the proceeds into another qualifying property.

The key word here, of course, is “defer” — not be confused with “permanently avoid.” As of this writing, it doesn’t appear that the new tax law has made any changes to the rules governing these exchanges, but because those rules are quite precise, it would be wise to keep an eye out for any new IRS guidance in this area.

Estate and Gift Taxes:

Estate taxes may not be a part of the day-to-day management of a property, but they can loom large in an investor’s long-term planning. Real estate can often be a high-value but illiquid asset, so that heirs could find themselves with a big tax bill but not the cash on hand to pay it — resulting in a rushed sale on unfavorable terms.

The new law raises the exemption to $15 million for an individual, or $30 million for a couple using portability. The exemption will be indexed for inflation, and it is permanent, i.e., it has no “sunset” date, as did the previous exemption. The new law did not repeal or amend the long-standing stepped-up basis rule. Under this rule, an heir receives property with a basis that equals the fair market value at the time of death. The heir can sell the property immediately with no capital gain (and no capital gain tax), or in the future the gain is just the increase in value since it was inherited.

Don’t lose sight of the fact that 12 states and DC impose their own estate taxes with varying exemptions and rates ranging from 8% to 20%, and 6 states have inheritance taxes with rates of about 1% to 18%. You may not be out of the woods quite yet.

SALT:

The infamous and often operatic debate over the State and Local Tax deduction resulted in an increase in that deduction from $10,000 per tax return to $40,000, reverting back to 10k in 2030. Perhaps less publicized is the PTET — Pass-Through Entity Tax, which allows pass-through entities like LLCs and partnerships to pay state income tax at the entity level, rather than passing that tax obligation through to individual owners. By doing so, this allows the entity to deduct the full amount of the tax as a business expense, effectively by-passing the SALT cap. The PTET is unchanged in the new tax law.

In conclusion:

The 2025 tax law brings a mix of permanent changes, updated incentives, and new planning opportunities that real estate investors will want to pay attention to. Whether it’s bonus depreciation, the QBI deduction, expanded Opportunity Zone benefits, or estate tax updates, these provisions could directly affect how you structure deals, manage your portfolio, and plan ahead. As always, it pays to run the numbers and work with trusted advisors—because good planning starts with good information.

Tools like RealData’s REIA software can help you project before- and after-tax cash flow with greater accuracy—so you can make better-informed decisions in a changing tax environment.

The information provided in this article is for educational and informational purposes only. It is not intended as, and should not be construed as, tax, legal, or investment advice. Every investor’s situation is unique, and the application of tax law can vary based on individual facts and circumstances. You should consult a qualified tax advisor, attorney, or financial professional before making decisions based on the information presented here.

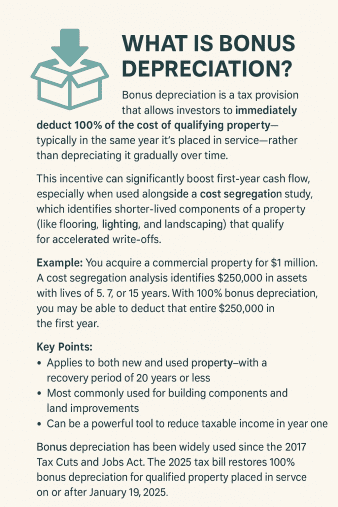

Bonus Depreciation:

Bonus Depreciation: