articles

A Practical Guide to Using AI for Real Estate Investment Analysis

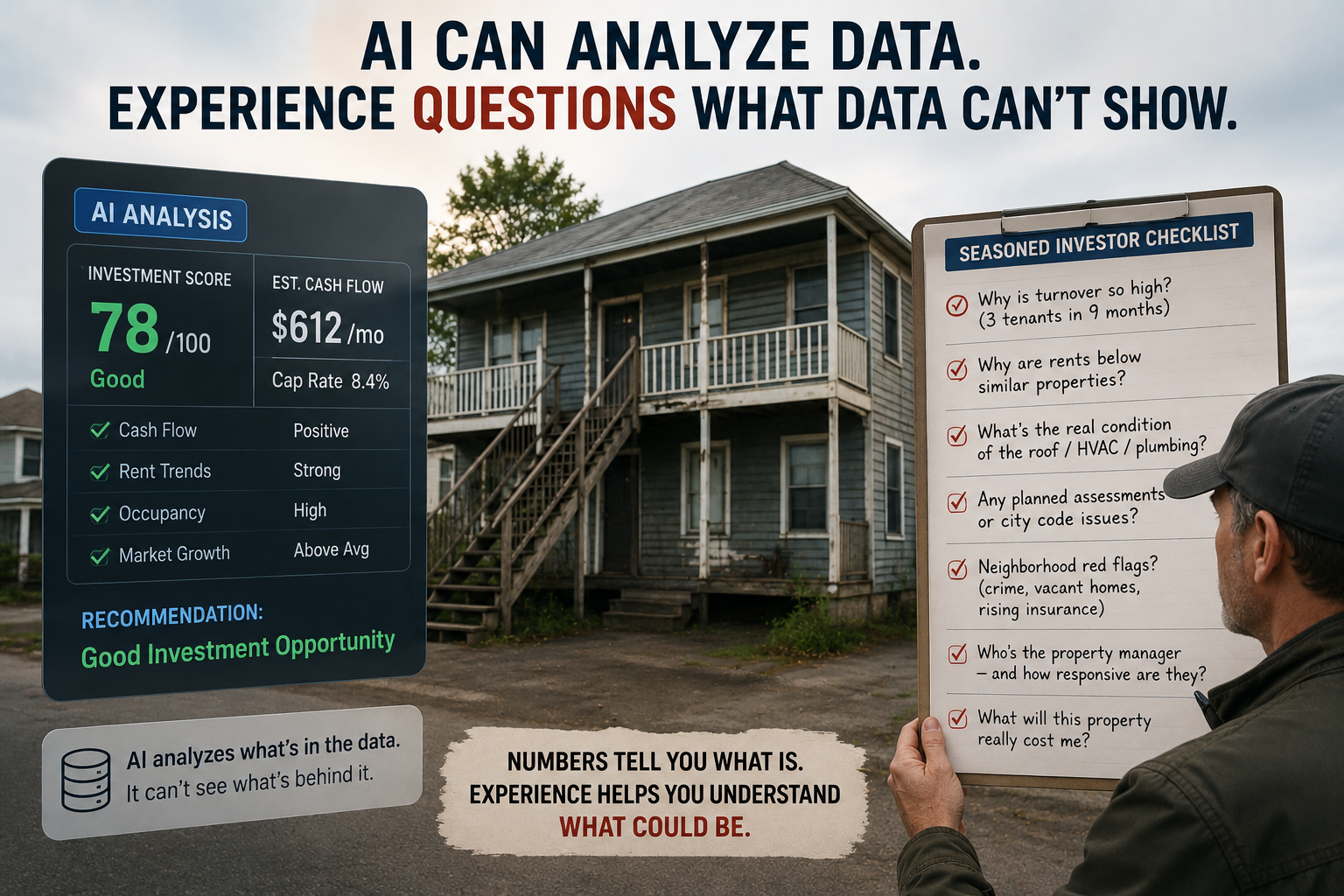

Give AI a properly constructed series of prompts and you get an operating statement you can check, a five-year projection, and an exit price. You also find out which assumption the return depends on, and that is is often not the one the broker is talking about. Here’s how this works on a realistic multifamily deal, a six-unit apartment building, and where the analysis pays for itself.